Cross-border payment inefficiencies threaten growth of Jamaican SMEs, regional data suggest

JAMAICA’S small and medium-sized enterprises (SMEs) confront significant obstacles in international trade due to costly, slow, and opaque cross-border payment systems — a challenge documented in a recent Mastercard white paper focused on Latin America and the Caribbean (LAC).

Although the report addresses the broader LAC region, the findings have direct implications for Jamaica’s entrepreneurial sector, which increasingly relies on international suppliers for business growth.

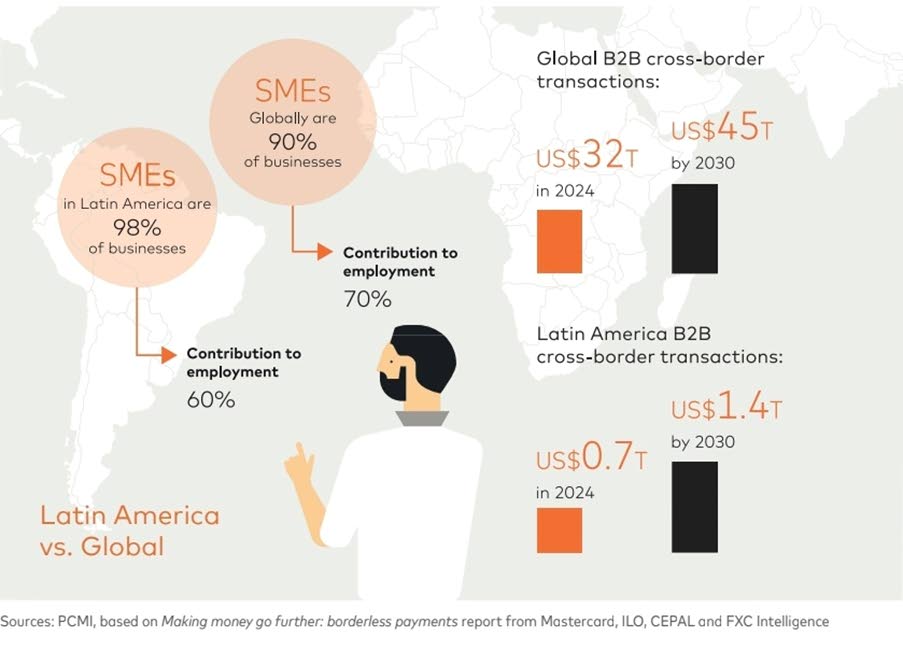

The 2025 Mastercard report, “Small businesses, big opportunity: Unlocking SME potential in Latin America’s cross-border space,” highlights that SMEs across the region represent about 98 per cent of businesses and provide 60 per cent of employment. Yet, despite their structural importance, they contribute a relatively low share of regional GDP, from 20 per cent to 35 per cent, reflecting persistent productivity gaps.

Latin American SMEs are engaging in cross-border trade at twice the global growth rate — 12 per cent annually versus 6 per cent worldwide — driven largely by expanding e-commerce and digital adoption. Although the report’s empirical study included Jamaica alongside Brazil, Mexico, Colombia, and others, direct data specific to Jamaican SMEs’ payment costs or timing details are not spelled out in isolation.

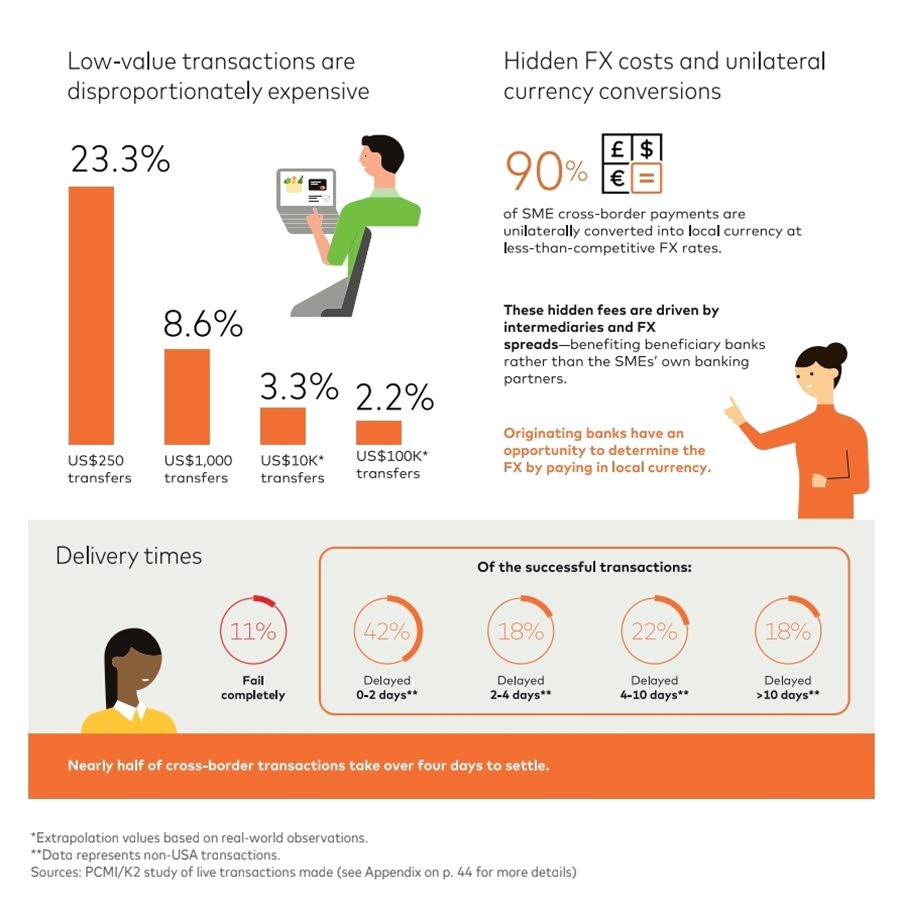

However, key regional trends are instructive for Jamaica’s business community. The report finds that low-value payments typical of SMEs, around US$250, incur fees averaging 23.3 per cent across LAC. Some corridors can see costs exceeding 30 per cent, challenging the viability of frequent small transfers critical to SME operations. In addition to that, 40 per cent of payments outside the US region take over four days to clear, with nearly 20 per cent delayed by more than 10 days. Brazil faces worse delays; Jamaica likely experiences similar systemic bottlenecks, given shared regional infrastructure constraints. The study also noted that approximately 90 per cent of payments denominated in US dollars convert automatically into local currency at less competitive rates without clear SME consent — a factor eroding the funds SMEs ultimately receive.

The study argues that these systemic inefficiencies stem largely from legacy correspondent banking infrastructures designed for multinational corporations rather than the agile and cost-sensitive demands of SMEs.

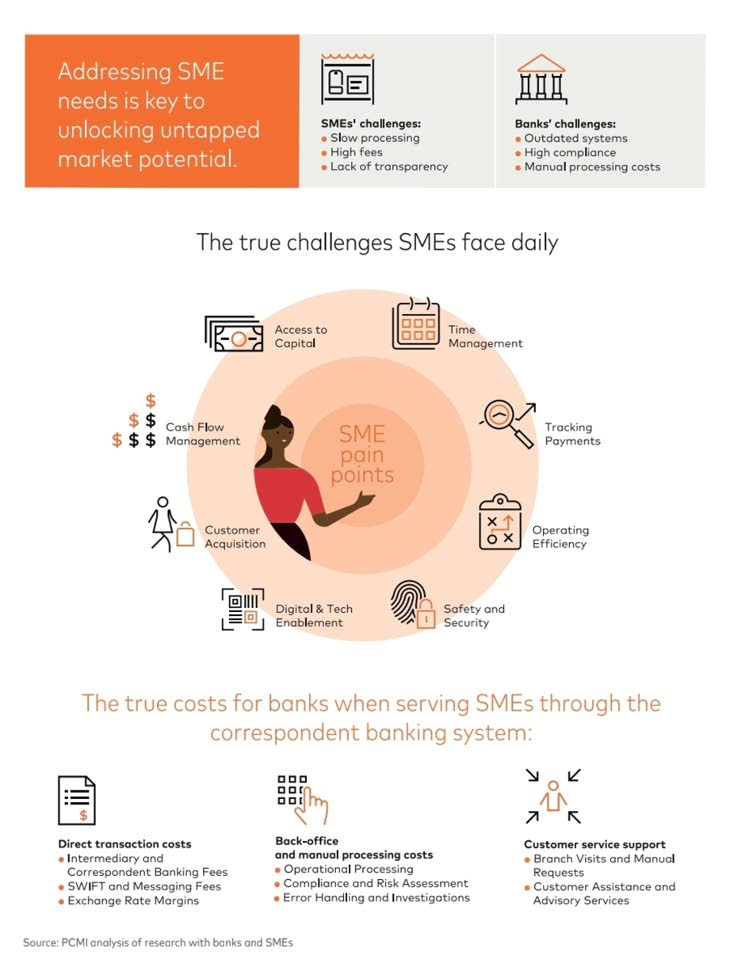

Jamaican SMEs, like their regional counterparts, operate without dedicated financial teams and are vulnerable to the effects of delayed payments, high fees, and lack of transparency. These conditions strain supplier relationships, disrupt cash flow, and inhibit international expansion efforts.

The Mastercard study underscores the urgency for banks to re-evaluate their SME strategies. Currently, banks retain 75 per cent of cross-border payment flows in LAC but face growing competition from fintech outfits offering faster, more transparent, and digitally integrated payment solutions. Banks cited high compliance costs, manual processing inefficiencies, and outdated systems as key operational hurdles in serving SMEs effectively.

Mastercard Move: A Potential Shift in the Cross-Border Payments Landscape

One response to the region’s payment system shortcomings is Mastercard Move, a platform designed to address some of the most acute pain points SMEs encounter in cross-border transactions. Unlike traditional correspondent banking, which often involves multiple intermediaries and associated costs, Mastercard Move uses a pre-funded local currency network model to facilitate international payments.

According to the white paper, this approach is intended to reduce intermediary layers, improve settlement times, and provide greater clarity regarding upfront fees and exchange rates. The system enables participating financial institutions to connect directly with local real-time payment and ACH infrastructures in over 120 countries. The report’s empirical assessment found that, for transactions processed through Mastercard Move, failure rates and delays were significantly reduced compared with conventional routes: in tests, only 2 per cent of payments reportedly failed versus the 11 per cent observed in traditional channels across the Latin America and Caribbean region.

The platform is designed to provide SMEs with real-time or same-day settlement options, advanced compliance tools, and digital integration features such as full payment tracking and self-service onboarding. These functions are increasingly demanded by businesses that have historically operated with less transparency, longer timelines, and higher costs.

Still, it is important to note that the white paper’s primary evidence base is a study limited to 70 SME transactions originating from eight countries (including Jamaica) and a series of stakeholder interviews. The scope, while illuminating, may not capture the full complexity and diversity of payment challenges for all SMEs in the region. Additionally, while Mastercard Move is featured as an example of innovation, the report does not provide granular independent field data on its performance specifically in the Jamaican market.

The report advocates five strategic shifts for banks to better serve SMEs:

(1) Segmentation of SME clients by real business needs rather than rigid size categories.

(2) A focus on solving operational cash flow and transparency challenges over pushing traditional products.

(3) Adoption of alternative, cost-effective payment rails suited for low-value transactions common among SMEs.

(4) Embedding payments within SME business tools such as invoicing and marketplaces.

(5) Provision of fully digital self-service capabilities offering real-time tracking and automated compliance.

It concluded that as global economic integration intensifies, strengthening cross-border payment systems is essential to unlocking SME potential in Jamaica and across Latin America. Banks and fintechs that respond decisively could capture emerging market opportunities while empowering the growth engines of local economies.

.

.

.