Budgeting back in focus as cost pressures mount

WITH inflation quietly eroding purchasing power and expenses climbing faster than wages, Jamaicans are being urged to rethink how they manage money, as budgeting discipline becomes increasingly critical in today’s high-cost environment.

While income levels vary widely, financial advisers argue that long-term progress depends not only on how much people earn but also on how much they retain.

“The focus should not be so much on how much you are earning, but rather how much you are keeping back, or saving,” said Carlton Stewart, assistant vice-president of retail sales and service at Barita Investments Jamaica, speaking during a Barita Money Talks Webinar.

His comments come amid mounting economic pressures reshaping household finances. Jamaica recorded strong growth in the September 2025 quarter, largely reflecting recovery activity following Hurricane Beryl. However, the subsequent impact of Hurricane Melissa is now projected to push the economy into contraction of about 4.3 per cent. The fiscal deficit is estimated at roughly 3.5 per cent of gross domestic product (GDP), with debt expected to rise to about 68.25 per cent of output. Economists estimate it could take three to five years for the economy to return to pre-Melissa levels, a period likely to keep cost-of-living pressures elevated. Against that backdrop, Stewart said many people ask how to begin investing without first addressing the more immediate question of where investment funds will come from. He noted that emotional spending patterns, particularly treating month-end income as discretionary money, often undermine financial plans before they begin. Failure to track day-to-day expenses, irregular costs and small recurring purchases also contributes to budget breakdowns.

“If you write down your budget, you will know what you can and can’t afford,” he said. “A budget is a written plan of how you will spend and tell your money where to go rather than having your money tell you what to do.”

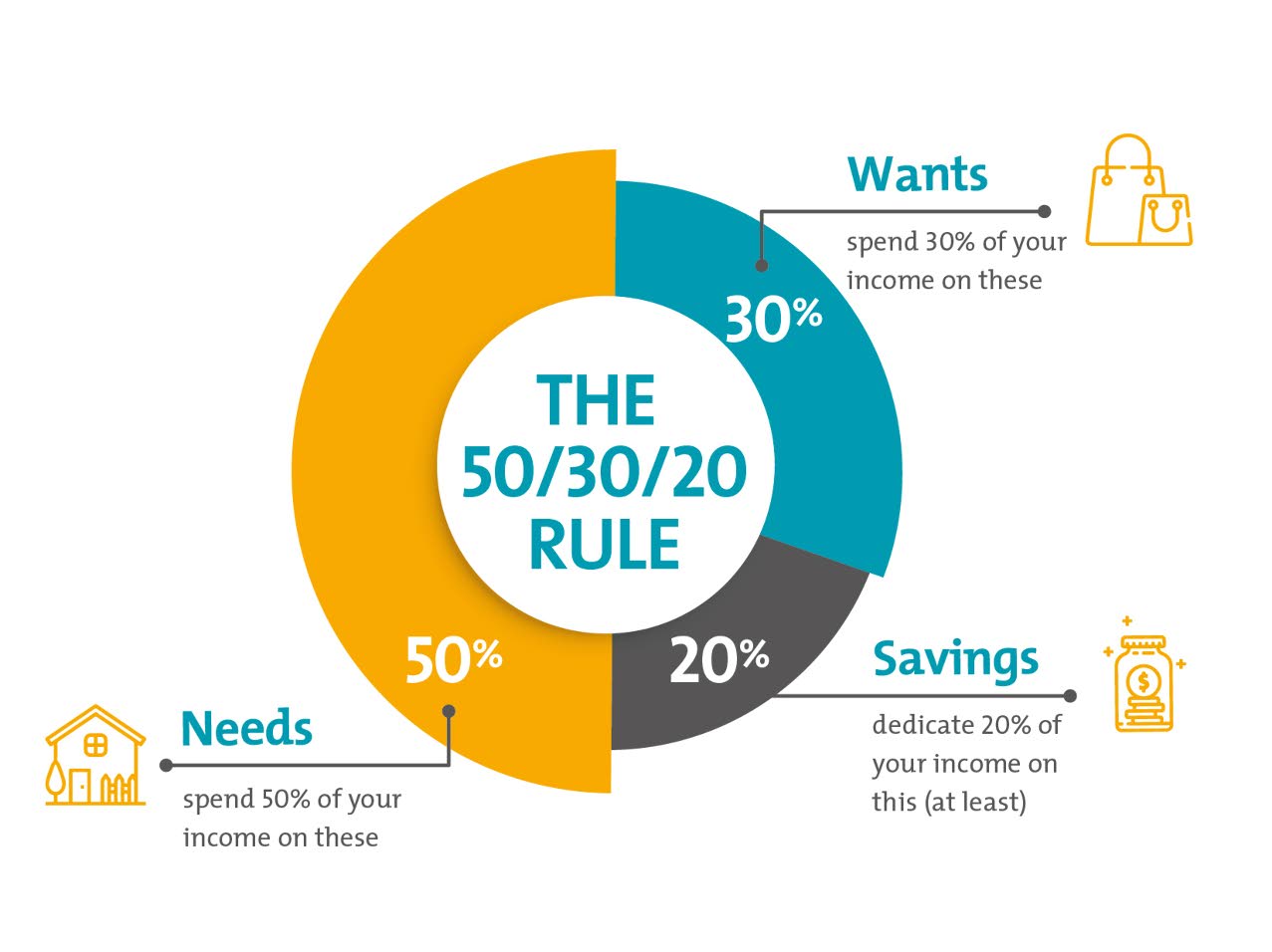

Stewart acknowledged that money habits are often shaped by early life experiences. Individuals who grew up in scarcity may hoard money out of fear, while others may overspend to compensate for past deprivation, both patterns that can hinder long-term wealth building. He also noted the warning signs that households may need structured financial guidance; these include depleted savings, mounting debt, absence of investments and reliance on a single income stream. He also pointed to the 50/30/20 budgeting framework, under which about 50 per cent of income goes to essential expenses, 30 per cent to discretionary spending and 20 per cent to savings and investment, which also includes pension contributions through employment.

“If the income is more than the expenses, that’s ideally where you want to be,” he said.

However, Stewart recognised that for many households expenses now exceed income as prices rise faster than wages. While reducing discretionary spending can help, he noted that some costs cannot realistically be cut.

“The reality is, you can’t go to your boss every month and request a salary increase,” he said. “So what do you then do? I want you to look at ‘How can I monetise my talent?’ and ‘How can I turn gifts I have into an income-generating opportunity for myself?’

He also addressed a common question among savers about the sequencing of debt repayment and investing. He advised building an emergency fund first, then prioritising high-interest debt such as credit cards before investing, noting the mathematical disadvantage of investing while carrying expensive debt.

“You have high mounting credit card debts at maybe 30 per cent or 38 per cent, but from an investment side you are averaging possibly eight per cent at its best; you are literally losing,” he said.

Lower-interest or income-generating debt, he added, may be compatible with investing strategies. As households navigate constrained finances, Stewart said budgeting should be viewed not as a restriction but as the foundation that determines whether saving and investing become possible at all.

The 50/30/20 budgeting framework allocates 50 per cent of income to essentials, 30 per cent to discretionary spending and 20 per cent to savings and investing, including pension contributions.

Tracking day-to-day and irregular expenses is a core step in budgeting discipline, financial advisers say, as unmonitored spending often undermines savings goals.