Gambling nation

Gaming tightens grip on $240-b gambling market as lottery share declines

JAMAICANS are wagering an estimated $240 billion a year, with machine-based gaming accounting for the largest share of spending even as lottery — the main source of government revenue — steadily loses share and sports betting expands.

The estimate is based on available quarterly data, as full-year figures have not been consistently published.

An analysis of Betting, Gaming and Lotteries Commission (BGLC) data covering 12 of the last 16 quarters to the end of 2025 shows the industry consistently generates between roughly $58 billion and $65 billion per quarter. That level of activity has remained broadly stable since the post-pandemic rebound in 2022.

While that points to the scale of the market, the regulator said a final figure is still being compiled. “Once all sales data have been fully compiled, reviewed, and verified, we will be in a position to provide an accurate assessment of the size of the market,” the BGLC said in response to Jamaica Observer queries.

Across the period reviewed, gaming — driven largely by machine-based play such as slot machines and other electronic gaming devices in licensed lounges and smaller route locations — accounted for the largest share of spending, typically between 56 per cent and 65 per cent. This reflects the high-frequency nature of machine-based gaming, where repeated, low-value bets accumulate quickly over time.

Lottery represented between 26 per cent and 35 per cent, while betting accounted for roughly 8 per cent to 11 per cent.

The direction of change, however, is clear.

Gaming has expanded in absolute terms, rising from about $29.3 billion in quarterly sales in early 2022 to roughly $39.4 billion by early 2025. Over the same period, lottery remained broadly flat, moving from about $18.7 billion to $19.2 billion, while betting increased from approximately $5.2 billion to $6.6 billion.

That shift has translated into a change in market share. Lottery’s share of total spending has fallen by roughly 5 to 7 percentage points over the period, slipping from about 35 per cent to below 30 per cent. Betting has edged up by around 1 to 2 percentage points, rising from under 10 per cent to just above that level.

The shift is subtle quarter to quarter, but consistent over time.

While the increase in betting remains modest, it is one of the few segments consistently gaining ground, suggesting a gradual reallocation of spending — particularly toward sports wagering — as lottery’s relative dominance declines.

Even so, gaming remains the central pillar of the industry, supported by its accessibility and high-frequency play model, which continues to anchor overall activity.

The structure of the market reinforces that dominance. Gaming activity is heavily concentrated in a narrow geographic corridor, with St Andrew and St James together accounting for between roughly 90 per cent and 96 per cent of gaming lounge sales across most quarters reviewed. St Andrew alone often contributes more than 60 per cent. This concentration means that performance in just a few parishes can disproportionately influence national outcomes.

That concentration reflects both population density and the clustering of licensed gaming locations in urban and tourism-linked areas, particularly Kingston and Montego Bay.

It also suggests limited penetration of machine-based gaming across the rest of the island.

The industry itself is served by a mix of licensed operators, including lottery promoters, multiple bookmakers, a single racing promoter, and several gaming machine operators and technical service providers, with activity in several segments concentrated among a small number of firms.

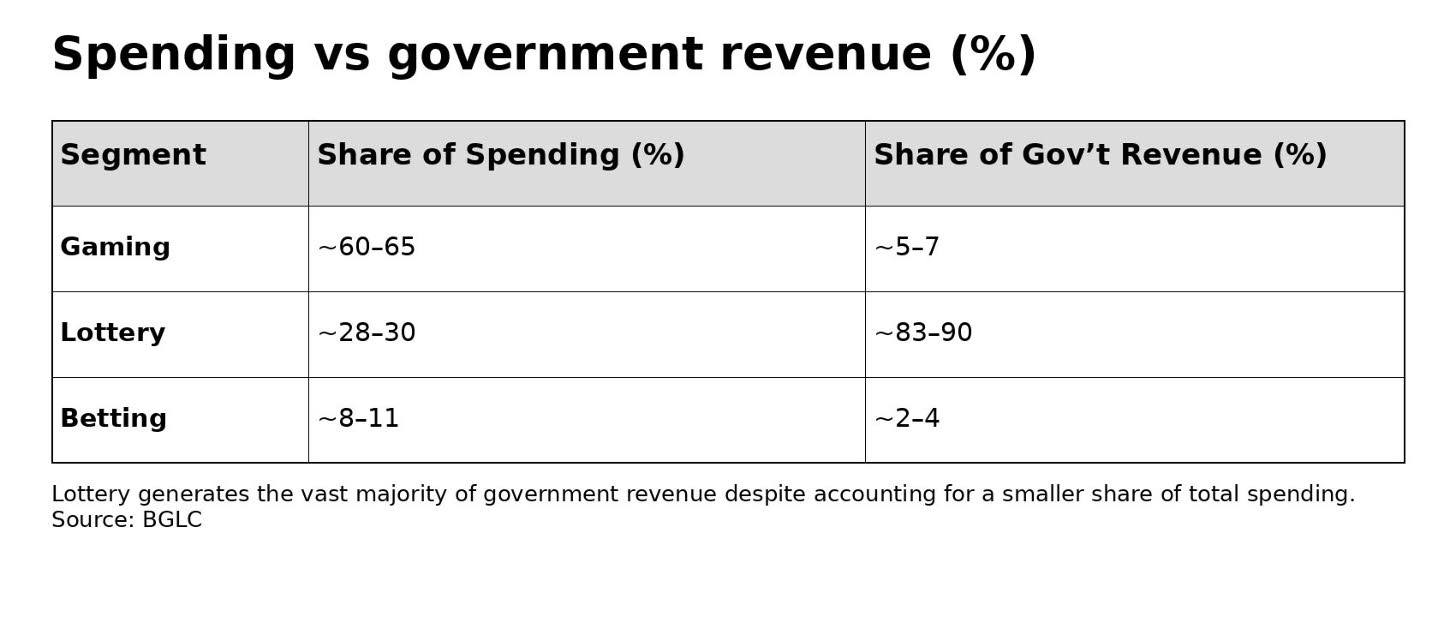

Despite gaming’s dominance in spending, the distribution of government revenue tells a different story.

Lottery, though smaller in overall activity, consistently generated between roughly 83 per cent and 90 per cent of government revenue across the period reviewed, while gaming and betting contributed far smaller shares, generally in the single digits.

That imbalance reflects the underlying economics of the segments. Lottery delivers higher margins, typically around 29 per cent to 32 per cent, while betting operates in the low 20 per cent range. Gaming, despite its scale, runs on much thinner margins, often below 6 per cent.

As a result, shifts in consumer spending toward gaming and betting do not translate proportionately into government revenue, leaving public finances tied to a segment that is gradually losing share. This creates a structural imbalance, where the fastest-growing areas of spending are not the main drivers of public revenue.

Industry growth was strongest in 2022, when quarterly sales rose sharply following the easing of COVID-19 restrictions, moving from about $53.2 billion in the January to March quarter to nearly $60 billion in the following quarter.

Since then, activity has stabilised, largely ranging between $61 billion and $64 billion through 2023 and early 2025, suggesting a transition from rapid post-pandemic recovery to slower, more steady growth.

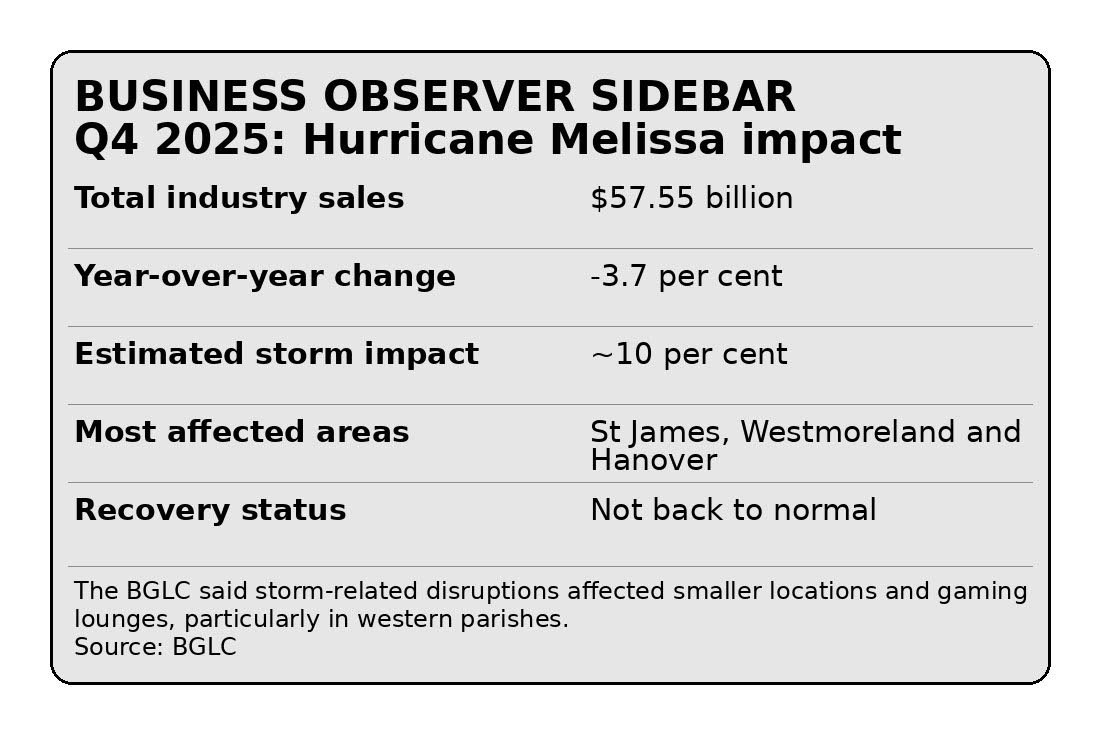

More recent data indicate some softening. In the October to December 2025 quarter, sales fell to about $57.55 billion, down 3.7 per cent from a year earlier.

The BGLC said “approximately 10 per cent” of that decline could be directly attributed to Hurricane Melissa, with “St James, Westmoreland and Hanover” among the most affected areas and activity “not returned to normal levels in these areas”. The impact highlights the sector’s vulnerability to external shocks, particularly in geographically concentrated markets.

Across the industry, payouts continue to absorb the majority of spending, typically between about 85 per cent and 88 per cent of total sales, leaving relatively thin margins overall.

Government revenue has remained broadly stable in nominal terms, generally ranging between about $2.3 billion and just over $3.1 billion per quarter, but the heavy reliance on lottery persists.

The commission acknowledged gaps in reporting, noting that quarterly performance reports have not been consistently published due to efforts to improve the “accuracy and completeness” of the data. It added that steps are being taken to support “a more standardised and predictable reporting schedule going forward”.

Taken together, the data point to an industry that has moved beyond its post-pandemic rebound phase and is now adjusting to shifting consumer behaviour. At the same time, the industry’s true size remains difficult to pin down due to gaps in reporting and incomplete quarterly coverage.

Spending is increasingly concentrated in gaming, betting is gradually expanding, and lottery’s role — while still central to government revenue — is steadily losing ground within the broader market.

.

Machine-based gaming now accounts for the largest share of gambling activity in Jamaica..