BANKS CASHING IN

Digital payments surge as fees rise, leaving Jamaicans paying more to move money

Key Points:

Banks are capitalising on Jamaica’s shift to electronic payments, with RTGS transaction volumes rising more than fivefold since 2018 even as cheque usage continues to decline sharply.

Customers are paying more to move money, as commercial banks maintain or increase digital transfer fees despite lower processing costs from the central bank.

The move to high-value electronic transfers is concentrating more transactions in fee-heavy channels, making transaction-based income an increasingly important revenue stream for banks.

COMMERCIAL banks are turning Jamaica’s shift from cheques to electronic payments into a growing revenue stream, with higher digital transfer fees leaving customers paying more to move money as transaction volumes surge.

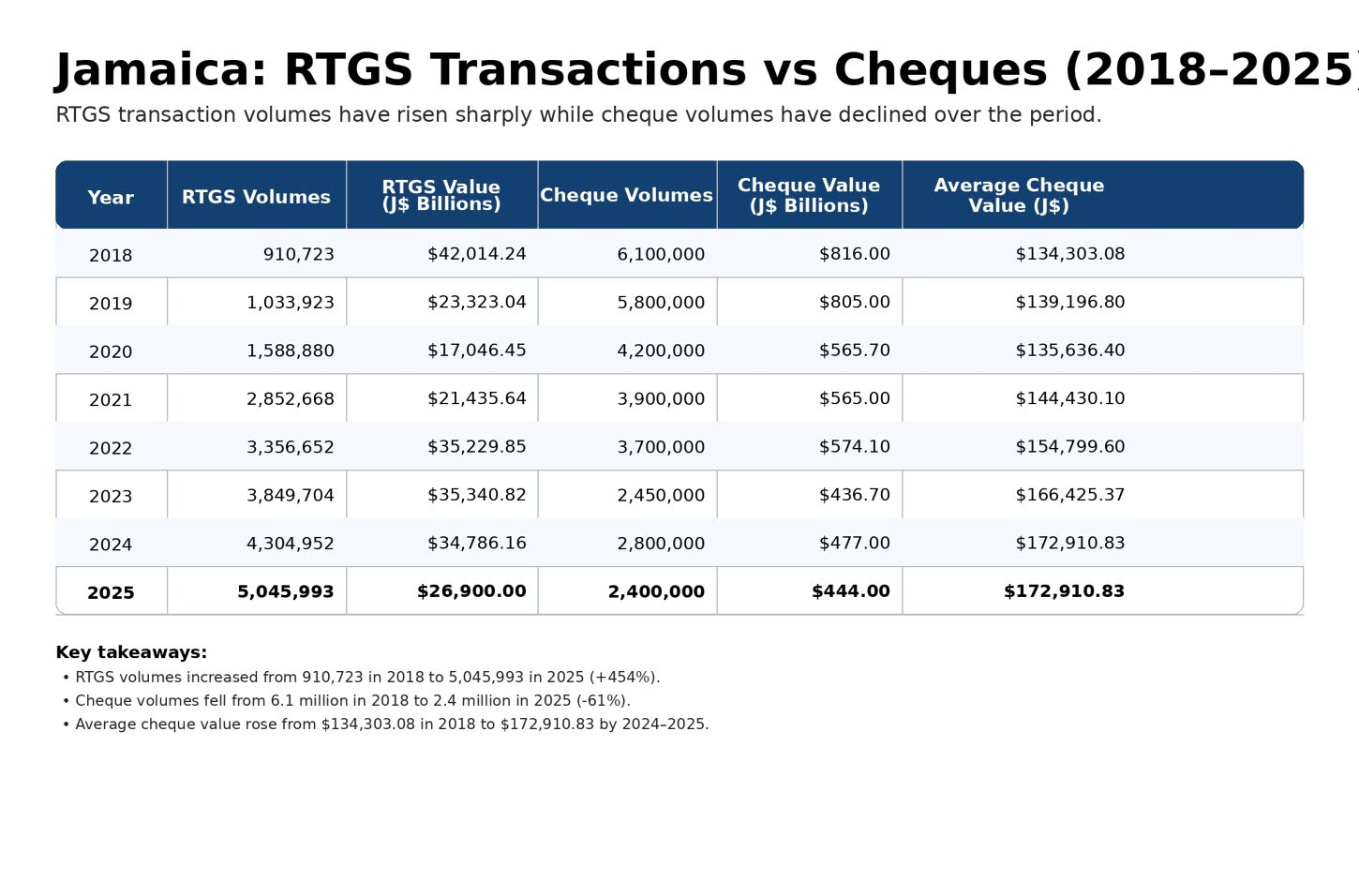

That shift is reflected in real-time gross settlement (RTGS) transactions, which rose from 910,723 in 2018 to 5.05 million in 2025, according to the Bank of Jamaica (BOJ).

“Growth in the JMD [Jamaican dollar] volume was largely attributed to an increase of 18.5 per cent in the number of participant payments on behalf of households and corporate clients,” the BOJ said in its 2025 annual report.

Cheque usage, meanwhile, fell from 6.1 million transactions in 2018 to 2.4 million in 2025, as more payments moved into electronic channels.

The value of RTGS transactions has been less stable, moving from $42 trillion in 2018 to $17 trillion in 2020 before rising again to $35.34 trillion in 2023.

This does not reflect a decline in demand for electronic transfers, but rather changes in the BOJ’s operations, including the elimination of the overnight deposit facility in 2019 for deposit-taking institutions (DTIs).

“This decline largely reflected a 33.5 per cent [$5.5 trillion] reduction in securities settlement transactions initiated in the JamClear®-Central Securities Depository (CSD) system, as a result of reduced demand for intraday liquidity to settle participants’ obligations,” the BOJ explained for the reduction in JMD RTGS values for 2025.

The long-term shift away from cheques has been steady. In 2010, 8.9 million cheques were processed through the automated clearing house (ACH) network, valued at $2.3 trillion.

By 2018, cheque values had fallen to $816 billion, and by 2025 to $44 billion.

“The decline in cheques processed may be attributed to changes in customers’ and financial institutions’ behaviour. Specifically, there was greater utilisation of electronic payment solutions as well as improved adherence to the ACH value threshold of $1.0 million,” the BOJ’s 2025 annual report noted.

Electronic transfers in Jamaica are conducted through the ACH network or the RTGS system. The ACH network is owned by Automated Payments Limited (APL) and operated by JETS Limited, with APL co-owned by DTIs, while the RTGS system is operated by the BOJ.

ACH transactions are generally low-cost or free for customers, with fees typically below $25. Under this system, the sender may pay a fee, but the recipient does not.

RTGS transactions, however, are structured differently. Both the sender and the recipient are charged a fee, making it a more expensive option for transferring funds.

According to a May 2022 advisory, the BOJ previously charged $100 per RTGS transaction to each participating DTI. That fee was suspended between March 2020 and April 2022 to encourage electronic payments, before being reinstated at a lower rate of $30 per transaction. Any amount above that is set by the individual financial institutions.

The BOJ’s own fees have declined, but charges to customers have not followed the same path.

The average incoming and outgoing online RTGS fees fell from $176.34 and $226.08, respectively, in December 2019 to $142.55 and $212.78 in December 2025. However, the fees charged by financial institutions remain broadly comparable to 2019 levels.

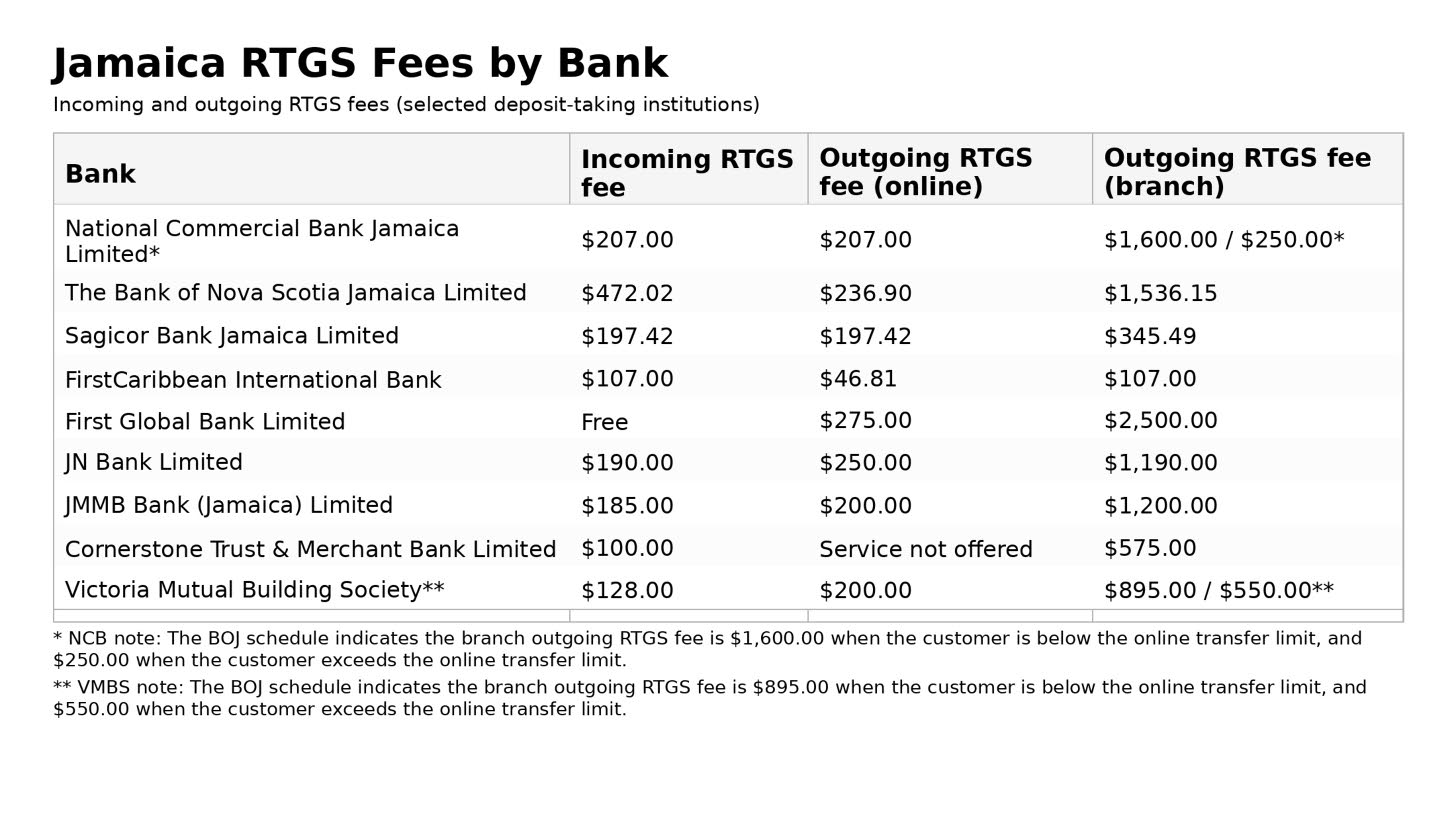

National Commercial Bank Jamaica Limited (NCBJ), the country’s largest commercial bank, previously charged $201.54 per transaction for incoming and outgoing RTGS payments in December 2019.

By December 2025, the incoming fee had increased from $95 to $207 per transaction.

The outgoing online fee rose from $160 to $207 for retail customers and from $198.95 to $207 for corporate clients. Corporate customers were not charged an incoming RTGS fee prior to November 2024.

The Bank of Nova Scotia Jamaica Limited (BNSJ), also known as Scotiabank Jamaica, previously charged $385 for incoming RTGS transactions in December 2019. That fee has increased to $472.02.

Its online outgoing RTGS service for personal customers, introduced in August 2024, is priced at $236.90 per transaction.

Corporate clients have seen outgoing fees rise from $385 in 2019 to $427.02 in December 2025.

NCBJ and BNSJ together control about three-fifths of banking assets in Jamaica, positioning them to capture a significant share of the fees generated from electronic transactions.

Other institutions are also adjusting their pricing. JMMB Bank (Ja) Limited will increase its outgoing online RTGS fee from $155 to $200 per transaction and its incoming fee from $100 to $185 effective April 17.

First Global Bank Limited (FGB) has raised its outgoing RTGS fee from $250 to $275 between 2019 and 2025, but remains the only DTI that does not charge an incoming RTGS fee. The bank also adjusted its fee schedule in November 2025 so that senior citizen accounts no longer pay an outgoing RTGS fee.

With transactions above $1 million required to pass through the RTGS system, a growing share of higher-value payments is being routed through a channel where fees are applied on both sides.

As a result, while the BOJ is collecting less per transaction, DTIs are capturing a wider spread on each electronic transfer offered to customers.

Even with the banking system losing out on nearly three months of RTGS fees following Hurricane Melissa, higher fees by some institutions have helped offset that gap.

The continued growth in electronic payments, combined with fee adjustments, is increasing the role of transaction-based income within the banking system while reducing reliance on cheque processing.

The BOJ completed the migration from the Swift Message Type (MT) standard to the ISO 20022 standard in December 2025, a move aimed at improving payment efficiency and interoperability.

“The successful completion of this transition marked the culmination of three years of preparatory work and represented a major milestone in modernising the national payments infrastructure and aligning the JamClear®-RTGS platform with international standards,” the BOJ said.

Commercial banks are earning more on digital transactions. (Photo: David Rose)

A table showing RTGS and cheque data from 2018 to 2025.David Rose

RTGS fees by the different banks. David Rose