Stable banks, shifting risk

How Jamaica’s lenders rewired who gets credit

Bank of Jamaica data show non-performing loans increasingly concentrated in households and real estate, while credit growth to agriculture and tourism lags the wider system – raising questions about what kind of economy the banking sector is really financing.

JAMAICA’S banks look safer than they did a decade ago. Bad loans are down from their post-crisis peak, capital buffers have improved, and total lending by deposit-taking institutions has more than doubled since 2017.

But a closer look at the Bank of Jamaica’s own numbers shows that financial stability has come with a quiet rewiring of who gets credit — and who bears the risk when the next downturn hits.

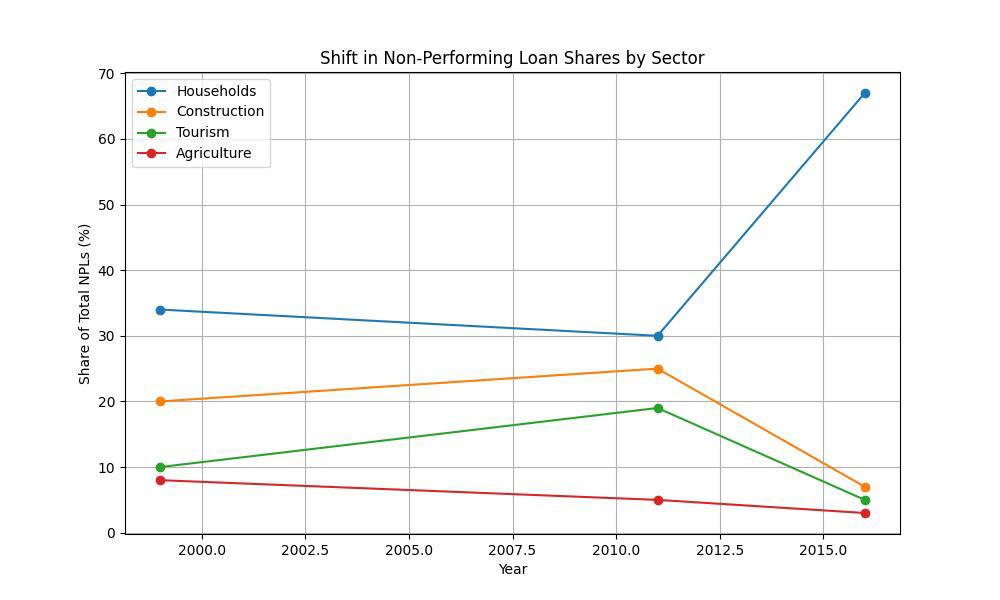

A long-run series of non-performing loans (NPLs) published by the Bank of Jamaica, covering March 1999 to December 2016, shows how credit stress has migrated across sectors over nearly two decades. A newer dataset, tracks the stock of loans by sector from March 2017 to November 2025. Taken together, they tell a story not just of cleaner balance sheets, but of a banking system that now leans much more heavily on household and property-related borrowing than in the past.

From balanced risk to household-heavy NPLs

At the turn of the millennium, bad loans were spread more evenly across the economy. In March 1999, total non-performing loans over 90 days past due stood at about $6.7 billion. Individuals and households accounted for roughly one-third of that (about 34 per cent), with the rest spread across sectors such as construction, agriculture, distribution and tourism.

By the time the system hit its post-global financial crisis peak at the end of 2011, the picture had changed dramatically. Total NPLs had climbed to just over $31.5 billion — nearly five times the 1999 level. Construction and tourism together accounted for almost 44 per cent of those bad loans, while households still represented close to a third. The spike was broad-based, but highly concentrated in a few stress-prone sectors.

What happened next was not simply a cyclical clean-up. By December 2016, the stock of NPLs had fallen back to around $18.4 billion. But the composition had shifted decisively. Households now accounted for about 67 per cent of all non-performing loans, more than double their share in 1999. Construction’s contribution had dropped to about seven per cent. Agriculture, manufacturing and transport were each down in the low single digits.

In other words, by 2016, the banking system’s residual credit problem was no longer spread across a range of business sectors. It was overwhelmingly lodged with individuals and households.

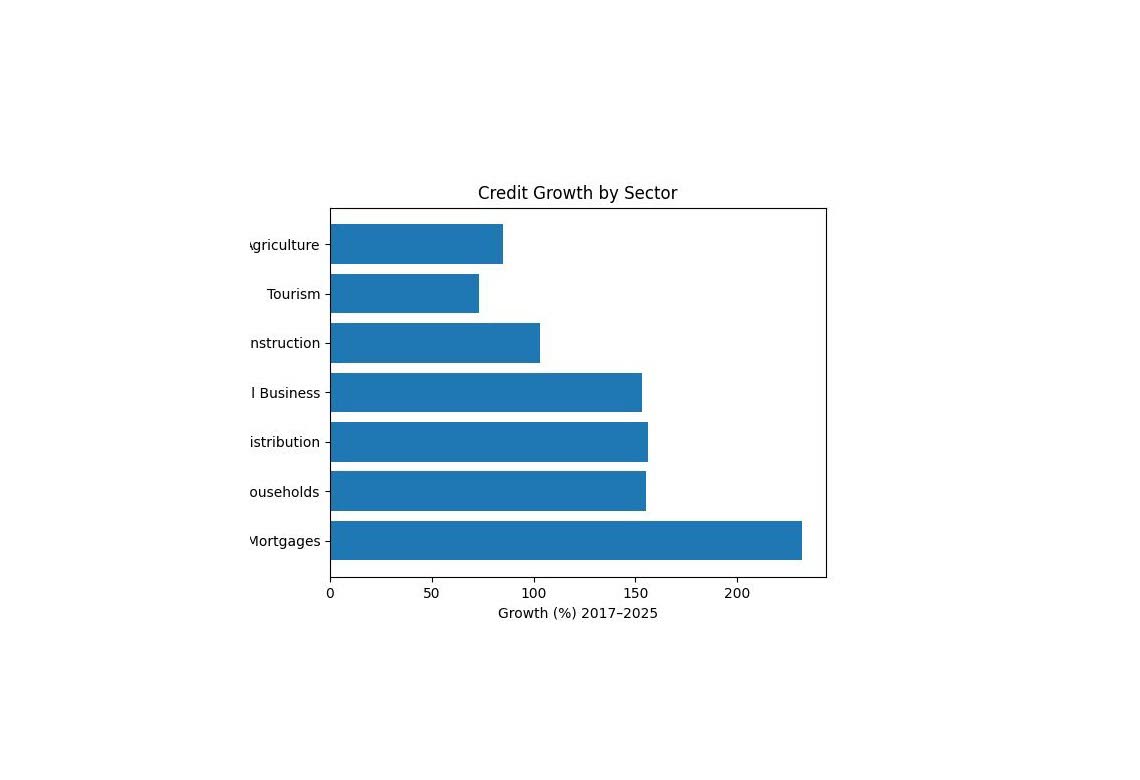

Loan growth has doubled down on households and property

The newer table, covering March 2017 to November 2025, shows what banks have done with their cleaner balance sheets.

Over that period, the stock of loans by deposit-taking institutions rose from roughly $659 billion to about $1.6 trillion, an increase of just over 142 per cent. Beneath that headline, though, some portfolios have grown much faster than others:

Individuals and/or households: up about 155 per cent, from roughly $333 billion to $848 billion.

Residential mortgages: up about 232 per cent, from around $157 billion in early 2017 to roughly $521 billion by November 2025.

Local business loans overall: up about 153 per cent, from roughly $220 billion to $558 billion, with especially strong growth in:

Distribution: up about 156 per cent (from roughly J$54 billion to J$139 billion).

By contrast:

Agriculture: up about 85 per cent, from about $8.6 billion to $15.9 billion.

Tourism: up roughly 73 per cent, from about $43.6 billion to $75.5 billion.

Construction lending has roughly doubled over the period — from about $27.6 billion to $55.9 billion — but still grew more slowly than mortgages and significantly slower than household credit overall.

The pattern is not of a banking system retreating wholesale from businesses. Local business loans have broadly kept pace with the system. Rather, the expansion has been tilted: towards households, housing and distribution-related activity, and away from some of the more volatile, export-linked or climate-exposed sectors.

A safer system – but safer for whom?

On their own, these shifts are not inherently good or bad. Households need mortgages and consumer finance; businesses depend on distribution chains; banks have to price risk.

But the combination of the two datasets raises awkward questions.

First, if households now generate most of the system’s residual NPLs, and banks have simultaneously expanded household and mortgage lending much faster than overall credit, future shocks will land more heavily on consumers and the property market than on traditional corporate borrowers.

Second, slower relative growth in agriculture and tourism — sectors that drive foreign exchange and rural employment — may be rational from a narrow risk-return perspective, but it also means the financial system is not leaning into some of the areas policymakers say they want to grow.

Third, the decline in the share of NPLs from construction and other historically risky sectors could reflect genuine improvements in underwriting and project quality – or simply lower exposure because banks have pulled back after the last crisis.

Without more recent NPL ratios by sector, it is impossible to say definitively which of these explanations dominates. But the direction of the numbers suggests that the banking system’s stability is increasingly anchored in the capacity of households to service debt and of the property market to hold its value.

Growth, inequality and concentration

There is also a broader development question.

Mortgage-led and consumption-heavy credit booms tend to feel good in the short run: house prices firm up, construction sites are busy, retail turnover is supported. But they do not always translate into the kind of productivity and export gains that raise long-term living standards.

The BOJ data show a system where:

credit to distribution and consumer-facing activity has grown faster than the loan book as a whole;

agriculture and tourism, which are more exposed to climate and external shocks, have grown more slowly; and

household debt has become both the main source of legacy bad loans and a rapidly expanding share of new credit.

That mix helps explain why banks can report strong prudential indicators even as parts of the real economy still feel under-financed or vulnerable to shocks.

For now, Jamaica’s banking system is widely seen as one of the country’s strengths: well-regulated, better capitalised, and less directly exposed to public-sector credit risk than in past decades.

The question hanging over the next cycle is whether the economy that system is financing — more leveraged households, more housing debt, relatively slower credit growth into some productive sectors — can deliver enough income, exports and resilience to keep those loans performing.

Financial stability, in other words, has been earned not just through better risk management, but by changing who gets credit and where the remaining risk sits. The data suggest that, increasingly, the answer is: with Jamaican households.