Oil shock squeezes reserve cushion

Rising oil prices and a wider import bill increase pressure on reserves and inflation

JAMAICA’S foreign reserves rose to US$6.91 billion at the end of March but the country’s import cushion appears far thinner than it did a month earlier, as the Bank of Jamaica (BOJ) revised how many weeks of imports those reserves can cover.

The latest figures from the central bank show net international reserves (NIR) increased by more than US$615 million in the first quarter, moving from US$6.29 billion at the end of December to US$6.91 billion at the end of March. At first glance, that suggests Jamaica is in a stronger position to absorb shocks. The picture, however, looks different, not because reserves suddenly fell, but because the BOJ changed the yardstick.

In its March 6 reserve report, the BOJ estimated that at the end of February the country had enough reserves to cover 56 weeks of goods imports and 36 weeks of goods and services imports, based on estimated import prices for the just-concluded fiscal year 2025/26. A month later, in the April 7 report, those same February reserves were restated using projected import prices for the current fiscal year 2026/27. Under that revised calculation, goods-import cover fell to 42 weeks, while cover for goods and services imports dropped to 28 weeks.

In effect, Jamaica appeared to lose more than 13 weeks of goods-import cover and just over eight weeks of overall import cover on paper — without reserves actually falling. From that revised February base, March’s coverage improved slightly to 43 weeks — nearly 10 months — for goods imports, and 29 weeks for goods and services.

Responding to questions from the Jamaica Observer, economist Keenan Falconer said Jamaica’s reserve position remains strong by international standards but the country’s exposure to repeated shocks means standard benchmarks do not tell the full story.

“The international benchmark is 12 weeks of adequacy, however this conceals several variations across different country circumstances,” Falconer told BusinessWeek. “Given our disproportionate vulnerability and frequent exposure to shocks, that may necessitate additional coverage. What might be adequate for most countries may not be similarly sufficient for a country with our economic realities,” he added.

Still, the central bank’s recalculation suggests it expects the import bill in the new fiscal year to be significantly higher than it was last fiscal year. Part of that heavier import bill may come from oil.

Global crude prices have climbed sharply since the recent escalation of conflict in the Middle East disrupted production and shipping routes. The US Energy Information Administration (EIA) said Brent crude, the global benchmark, averaged US$103 per barrel in March and is expected to climb as high as US$115 per barrel in the second quarter, before easing later in the year. The agency said uncertainty around future supply disruptions is likely to keep prices above pre-conflict levels.

“It is important to note that the adequacy coverage is measured using the current value of imports. So if the value of imports rises substantially, as in the price of oil and other commodities, then the number of weeks of coverage declines,” Falconer pointed out.

“To further illustrate the point, at the end of February, prior to the recent spike in oil prices, NIR was US$6.8 billion and sufficient to cover 36 weeks of imports of goods and services. At the end of March the NIR increased to US$6.9 billion. However, because of the oil price spike in recent weeks, coverage has declined to 29 weeks,” Falconer added.

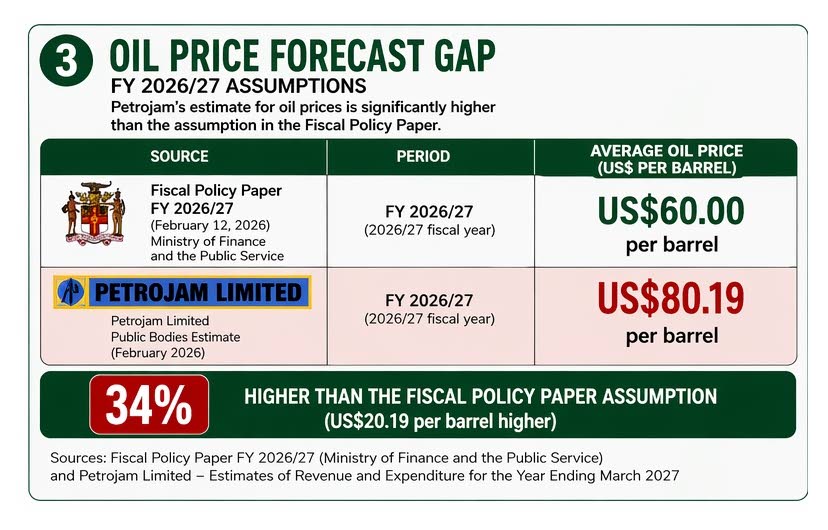

Yet even before this latest oil price spike, some official projections may have understated the risk. In the Government’s Fiscal Policy Paper for fiscal year 2026/27, average oil prices are forecast to increase 3.6 per cent to US$60 per barrel relative to the previous fiscal year. But in the Public Bodies Estimates, Petrojam projects an average crude acquisition price of US$80.19 per barrel for the same period. That is roughly 34 per cent higher than the Government’s assumption. If Petrojam’s projection proves closer to reality, Jamaica’s import bill could rise faster than current official forecasts suggest, putting added pressure on inflation, the current account, and the reserve position.

Some of that pressure is already showing up at the pumps for consumers in Jamaica. State-owned oil refinery Petrojam, the country’s main fuel price-setter, raised gasolene prices by $4.50 per litre in four consecutive weeks during March, with another $4.50 increase announced for this week, even as some diesel prices eased marginally.

Those higher fuel and energy costs are already showing up in inflation. The Statistical Institute of Jamaica (Statin) said consumer prices rose 0.3 per cent in March, driven partly by a 0.6 per cent increase in transport costs due to higher petrol prices while the ‘Housing, Water, Electricity, Gas and Other Fuels’ division rose 2.3 per cent, largely because of higher electricity rates. Point-to-point inflation moved up to 4.3 per cent in March from 3.9 per cent in February.

The Bank of Jamaica’s Monetary Policy Committee (MPC) in February did not explicitly build higher oil prices into its main forecast but noted that “the MPC also considered external risks related to oil prices and global financial conditions”.

The committee projected Jamaica’s current account would move from a broadly balanced position in fiscal year 2025/26 to a deficit of 6 to 7 per cent of GDP in fiscal year 2026/27. Net international reserves are also projected to fall to US$6 billion after ending fiscal year 2025/26 at US$6.8 billion.