Shareholders miss out on $17 dividend as Carib Cement parks cash with Cemex

Caribbean Cement Company Limited (CCC) has built up $15.7 billion in cash, but much of it is being channelled to its parent, Cemex, rather than paid out to minority shareholders.

CCC paid $1.73 billion in dividends to shareholders during 2025, with $1.41 billion paid to Trinidad Cement Limited (TCL) and Cemex Operaciones México, S.A. de C.V. While this represents a 30 per cent dividend payout ratio based on 2024’s net profit, the company has been placing its accumulated cash with a related company rather than paying more dividends.

CCC had $15.1 billion (US$94.9 million) in a deposit investment account with CEMEX Innovation Holding Limited (CIH), a Swiss company, as of March 31. CCC earns interest on this cash at the secured overnight financing rate (SOFR) plus 0.30 percentage points. It began depositing this cash with the Swiss company in the first quarter of 2022 after becoming debt-free in 2021.

This means that the cement manufacturer keeps approximately $600 million in Jamaica to support its ongoing operations and cover any unclaimed dividends for minority shareholders. While this move creates the opportunity for CCC to earn four to five per cent on its cash pile, it also highlights the strategy being undertaken by its ultimate parent company to manage subsidiary cash.

When CCC paid its $1.73 billion ($2.0979 per share) dividend in 2025, Cemex Operaciones México received a gross amount of $88.51 million while TCL received a gross amount of $1.32 billion. Due to the Caricom double taxation treaty, those funds paid to TCL are not subject to withholding taxes, while Cemex Operaciones México is subject to a ten per cent withholding tax.

If TCL were to distribute all the dividends it received from CCC to its shareholders, Cemex would only receive 69.83 per cent, or $923.76 million, via its subsidiary Sierra Trading. So, from the original $1.73 billion paid by CCC, just $1.003 billion, or 56 per cent, would ultimately reach Cemex via its wholly owned subsidiaries Sierra and Cemex México.

By having CCC park its cash with Cemex Innovation, Cemex pays a small cost to CCC as interest while retaining access to those funds for its broader operations. CCC’s notes state that the investment account “is considered highly liquid and is classified as a cash equivalent because the funds can be withdrawn at any time with minimal notice.”

During the first quarter ending March 31, CCC generated $4.05 billion in cash, nearly triple the $1.21 billion generated a year earlier. However, the company’s balance with Cemex Innovation moved from $11 billion to $15.1 billion during the quarter, meaning that most of the cash generated was transferred to the related entity.

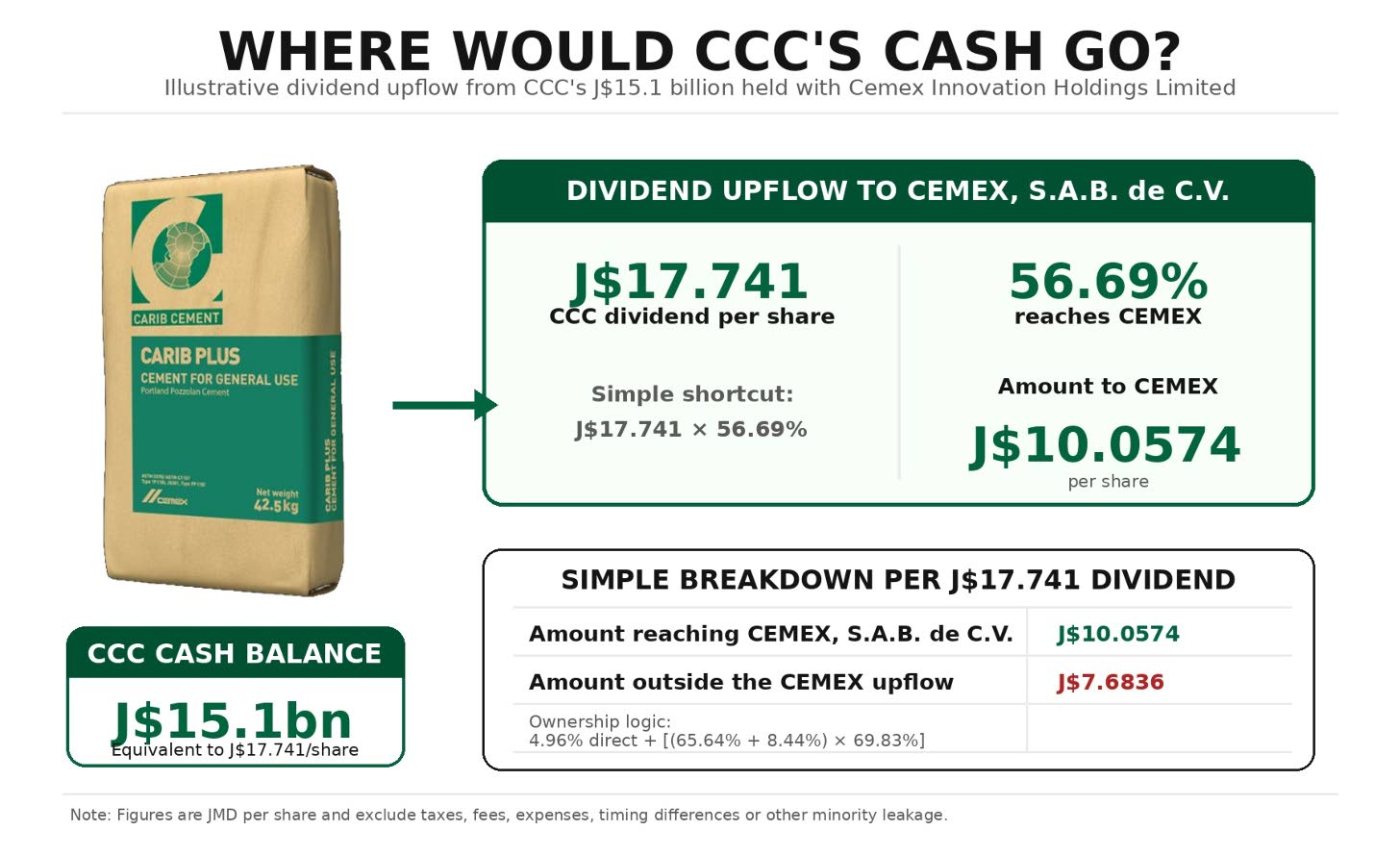

If CCC were to pay that entire $15.1 billion balance as a dividend to shareholders, it would amount to $17.74 per share. Based on the $102.59 closing price, that’s a 17.29 per cent dividend yield for shareholders. However, Cemex would receive $1.01 billion after it flows through TCL and Sierra.

Due to the Master Services and Intellectual Property Agreements signed in January 2022, Cemex’s subsidiaries collectively receive three per cent of the company’s consolidated net sales. Cemex charged CCC two per cent between 2022 to 2024 before increasing it in 2025 to three per cent. That agreement has a four per cent cap and is set to automatically renew in January 2027 for another five years.

Cemex received $2.22 billion as royalty and service fees between 2022 to 2025 under this master agreement. So, that Cemex logo on the bag isn’t just there for aesthetics but also represents a recurring cost the company pays every year to its main shareholder.

CCC leverages bargaining power

Due to CCC being the country’s sole cement manufacturer with strong cash generation and no debt, it holds significant bargaining power with its suppliers. This means that it might have credit terms ranging from a few days to months.

As part of its strategy to support cash management, CCC has a supplier finance arrangement where banks will pay a supplier early by factoring their receivables owed to the cement company. This means in practice that a supplier will sell its receivable at a discount to a bank and get paid early, while a bank will collect the full amount from CCC at a later date. That difference represents profit to the bank.

This balance stood at $1.39 billion, or 42 per cent of the company’s trade payables, in 2022. That balance has risen to $3.45 billion, or 63 per cent of the company’s trade payables, in 2025. This strategy allows the company to manage payables on its own terms while controlling the timing of cash outflows.

“Under the arrangement, the banks agree to pay an amount to participating suppliers in respect of invoices owed by the Group and receive settlement from the Group at a later date. The principal purpose of this arrangement is to facilitate efficient payment processing and enable willing suppliers to sell their receivables due from the Group to the banks before their due date,” CCC’s 2025 audited financials stated.

CCC reports record earnings

Following the company’s US$42-million ($6.7-billion) expansion, or debottleneck project, in 2025, CCC reported a 13 per cent rise in consolidated revenue to $9.26 billion. With cost of sales remaining flat, gross profit jumped 25 per cent to $4.71 billion, representing improved margins driven by tighter material costs.

Tight expense control and improved interest income resulted in operating profit growing 31 per cent to $3.53 billion. Profit before tax increased 28 per cent to $3.54 billion, with lower taxes resulting in net profit rising 53 per cent from $1.99 billion to $3.05 billion. This is the highest first-quarter net profit in the company’s history.

The profitability of the first quarter was equal to more than half of the $5.92 billion in net profit reported in 2025. CCC has $29.92 billion in property, plant and equipment, which represents the investment made into its Rockfort plant and machinery. It had $3.33 billion in inventories, representing raw material and finished product to be sold. CCC had $35.52 billion in shareholders’ equity relative to $49.71 billion in total assets as of March 31.

TCL highlighted in its own first-quarter report that CCC represented 96 per cent of its Q1 operating profit of TT$171.65 million ($3.99 billion). This contrasts with Trinidad at TT$1.27 million and Guyana and Barbados combined at TT$5.98 million. This demonstrates the importance of CCC to TCL’s capital structure, but also the constraints in moving the asset directly under Cemex’s ownership.

“As 2026 unfolds, the company anticipates continued strong performance, while remaining mindful of risks, including higher fuel and energy costs from the US–Iran conflict. Proactive measures will be taken to mitigate any long-term impacts and maintain operational stability,” CCC said in its Q1 report.