Credit unions move closer to payments big league

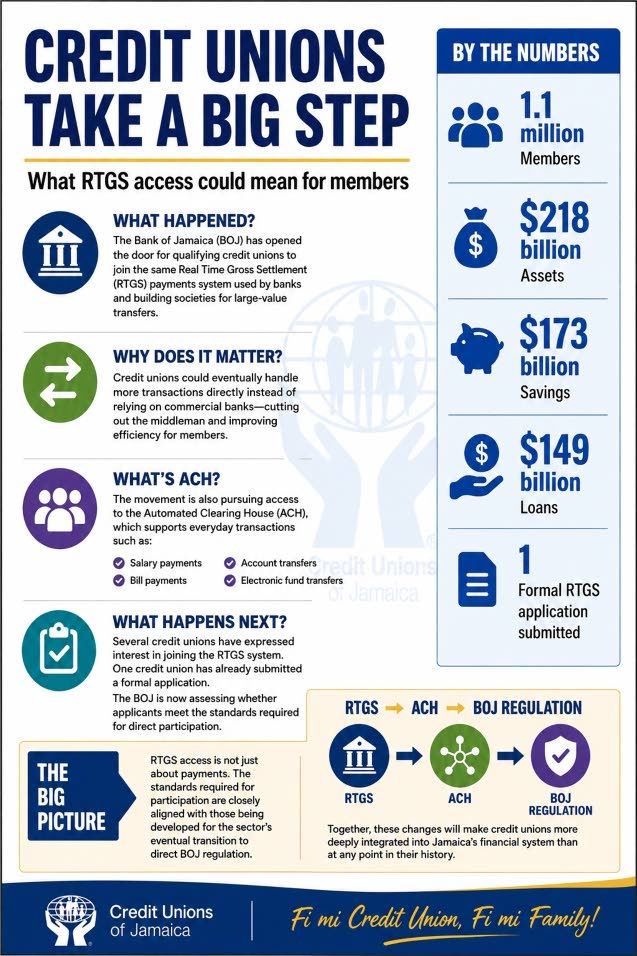

MORE than one million Jamaicans who belong to credit unions could eventually see faster electronic transactions and wider payment services after the Bank of Jamaica (BOJ) opened the door for qualifying credit unions to connect directly to the country’s real-time payments system, reducing their reliance on commercial banks to move money.

The policy change, which took effect on May 12, revised BOJ’s JamClear Real-Time Gross Settlement (RTGS) policy to make credit unions eligible for direct participation in the system already used by banks, building societies, and other financial institutions to process large transfers that are completed almost immediately.

Jide Lewis, BOJ deputy governor with responsibility for financial institution supervision, told the Jamaica Observer that several credit unions have expressed interest in participating, and one institution has already submitted a formal application. The central bank is reviewing that application and gathering information from other interested institutions.

For Jamaica’s credit union movement, the change represents a step towards handling more transactions directly instead of relying on commercial banks as intermediaries.

“We’re pretty much cutting out the middleman,” Andrea Messam, immediate past president of the Jamaica Cooperative Credit Union League (JCCUL), told Sunday Finance in an interview on the sidelines of the organisation’s 85th annual convention and annual general meeting at Ocean Coral Spring in Trelawny on June 5.

The policy change comes as the movement continues to grow in size and financial weight.

At the end of March the movement reported 1.1 million members, assets of $218 billion, savings of $173 billion, and loans of $149 billion. Membership increased by more than 8,000 during the first quarter while assets grew by $4.3 billion.

Credit unions have generally had to rely on commercial banks to access some payment systems. Direct participation would allow qualifying institutions to connect for themselves.

Messam said the move is part of a broader effort to expand the sector’s role in electronic payments.

She noted that the credit union movement is also working towards participation in the automated clearing house (ACH) network, which handles many of the routine electronic transactions consumers use every day, including salary payments, bill payments, and transfers between accounts.

For members, the more visible change may come later through ACH. RTGS access would help credit unions process large-value transfers more directly, while ACH participation would bring the sector closer to the everyday payments infrastructure used by banks.

Together, RTGS and ACH would give credit unions greater access to the systems that support both large financial transfers and routine electronic payments.

Speaking at the convention, Lewis said the RTGS policy revision followed discussions with the credit union movement which had been advocating for direct access to the systems used to move money between financial institutions.

“You spoke. We listened,” Lewis told delegates.

Lewis said the change reflects the growing size and importance of the credit union sector within Jamaica’s financial system, noting that the sector accounts for roughly 6.5 per cent of assets in the deposit-taking sector and about six per cent of gross domestic product.

“Your reach is massive,” he said.

“You have over a million members across all your entities and that means that you are systemically important because you’re too widespread to fail.”

.

The significance of the RTGS decision extends beyond payments. Lewis said that once the new regulatory framework for credit unions is in place, qualifying institutions could gain access to certain BOJ funding facilities if they run short of cash.

That means eligible credit unions could potentially borrow from the central bank for a short period if they face unusually high withdrawal demands from members, provided they have assets to back the loan.

Lewis used the example of a natural disaster or a sudden rush by members to withdraw funds.

“The idea is that we’ll be able to, at a click of a button, make available to that impacted credit union a six-month lending facility,” he said.

Participation, however, will not be automatic.

Lewis said credit unions seeking direct access must show they are financially sound, well managed, and capable of operating safely within the payments system.

“Access is not merely a technical matter,” he said, adding that institutions must be capable of meeting the standards expected of participants in a systemically important payments network.

Lewis said the requirements for RTGS participation are closely aligned with those being developed for the sector’s eventual transition to BOJ regulation.

“The same criteria that we’re looking for to make you eligible to receive a licence are really going to be the same things that we’re looking for, for you to access the payment system,” Lewis said.

The opportunities created by greater access to the payments system come at a time when the movement is also facing some challenges.

While assets, savings and loans continued to expand during the first quarter, delinquent loans increased to $9.44 billion from $8.19 billion at the end of December. The delinquency ratio rose to 6.31 per cent, above the movement’s target of five per cent.

Lewis also warned that stronger governance must be matched by investments in technology and cyber security.

He said that as commercial banks strengthen their defences, cyber criminals are increasingly turning their attention to other parts of the financial system, including credit unions.

“What we’re trying to say this afternoon is because we have forced the banks to tighten their internal control environment, that makes it harder for criminals to defraud banks [so] it now means that they’re going to turn their attention to the credit union sector,” he said.

For most members, the changes will not be immediately visible but over time they could influence how salaries are paid, how bills are settled, how money moves between accounts, and how credit unions compete with other financial institutions.

The RTGS decision is only one step, but combined with the push for ACH participation and eventual BOJ regulation, it points to a larger change in how credit unions may serve more than one million Jamaicans — not only as lenders and savings institutions, but as fuller participants in the country’s payments system.