SCOTIA’S $54-B EXIT PROBLEM

Proposed buyout removes one of the JSE’s largest dividend stocks; investors with few options

JAMAICAN investors could receive about $54 billion from the proposed buyout of Scotia Group Jamaica Limited, one of the largest dividend-paying companies listed on the Jamaica Stock Exchange (JSE), but replacing it may prove harder than finding somewhere to park the cash.

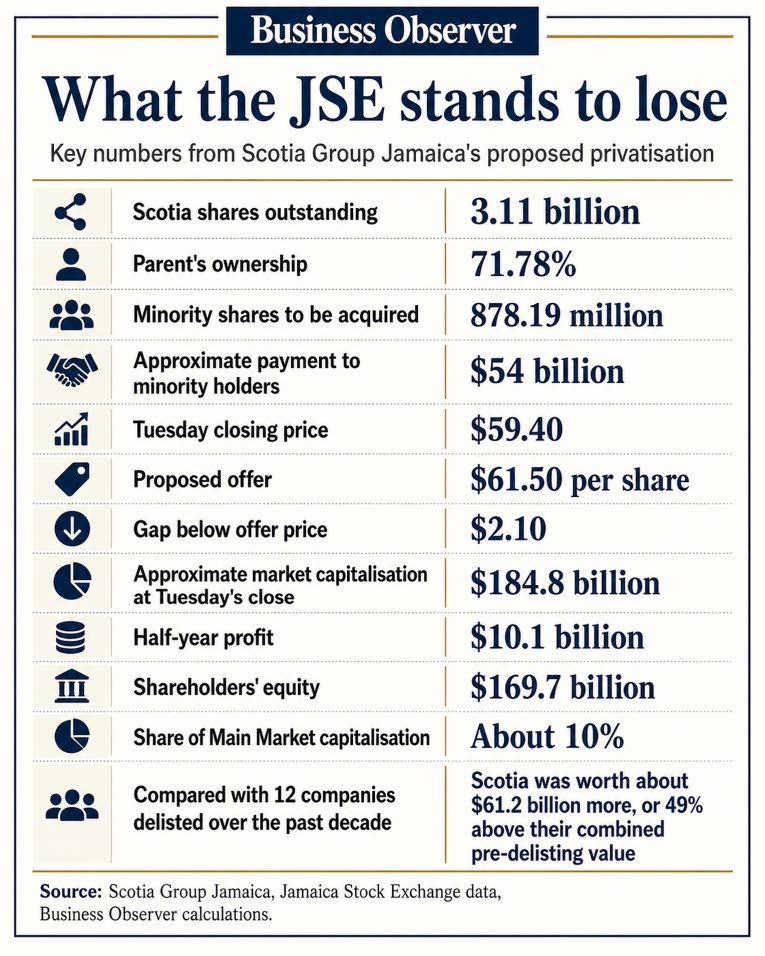

Scotiabank Caribbean Holdings Limited, which owns 71.78 per cent of Scotia Group, has offered $61.50 per share for the shares it does not already own as part of a plan to take the banking group private.

The offer values the minority stake of more than 878 million shares at approximately $54 billion. Scotia’s stock rose 82 cents, or 1.4 per cent, to close at $59.40 on Tuesday, leaving it $2.10 below the proposed purchase price. At that market price, the company was valued at about $184.8 billion.

If approved, the transaction would give pension funds, unit trusts, other large investors and individual shareholders a substantial cash payout. It would also remove a major financial stock from a market with relatively few companies large and liquid enough to absorb significant institutional investment.

Richardo Williams, senior vice-president for asset management and head of Barita Fund Managers, said the proceeds are unlikely to be reinvested in any one place.

He said some of the money could flow into other Jamaican stocks, while some may go into bonds, overseas investments or other assets, depending on each investor’s mandate, risk limits and the returns available at the time.

Although the JSE may appear large enough on paper to absorb some of the payout, Williams added that the choices available to major investors are much narrower in practice.

“The binding constraint is less likely to be the existence of listed equities and more likely to be investable capacity under investment mandate and risk limits,” he said in emailed responses to questions from the Jamaica Observer.

Put simply, other stocks may be available, but large funds cannot always buy as many shares as they want.

Williams explained that pension funds and unit trusts cannot put too much money into one company or industry. They must also find enough shares for sale without pushing the price up sharply.

As a result, even a company listed on the JSE may be too small, too rarely traded or already too heavily represented in a fund’s portfolio to take in a large investment.

Hard to replace

Williams said investors may need several assets to reproduce the role Scotia played in their portfolios.

“The question is not necessarily whether Scotia can be replaced by another stock, but rather whether its role within a portfolio can be replicated,” he said.

For many investors, Scotia offered several benefits at once: regular dividend income, exposure to the financial sector, a record of profitability and the ability to trade meaningful quantities of shares.

Investors may therefore have to spread their Scotia proceeds across several stocks, bonds and other investments to recreate that mix.

Scotia reported net income of $10.1 billion for the six months ended April 30, up from $9.2 billion a year earlier. Its board also approved a second interim dividend of 45 cents per share.

Scotia Group Jamaica Limited’s headquarters in downtown Kingston. The banking group’s majority shareholder has proposed buying out minority investors and taking the company private.

Davie Martin, general manager for trading and treasury at JMMB Group, said Scotia’s departure would reduce the choices available to investors seeking regular dividends and a stock that trades often enough for them to enter or leave sizeable positions.

Martin noted that about 26.4 million Scotia shares changed hands in 2025, compared with more than 117 million NCB Financial Group shares and 19.6 million Sagicor Group Jamaica shares.

He pointed out that many Scotia shares are held by pension funds and other long-term investors, meaning only a smaller portion may be available for trading at any given time.

Scotia’s shareholder report shows that its 10 largest shareholders control more than 82 per cent of the company, including the parent company’s 71.78 per cent stake. The other major holders include pension funds, pooled funds and investment accounts.

“If the deal goes through, then minority shareholders will have to seek appropriate alternative investment options, which could be difficult, especially in the sizes required by institutional investors,” Martin said in responses to

Business Observer.

Pressure on remaining large stocks

Williams noted that if a large share of the payout remains in Jamaican equities, more money could begin chasing the relatively small number of companies large enough for major investors.

He said that could push up the prices of some remaining blue-chip stocks, while increasing the amount of money concentrated in a few companies. Higher prices could also reduce the dividend yield available to new buyers unless those companies raise their payouts.

Williams added that the final effect would depend on how investors divide the proceeds among local shares, bonds, overseas investments and other assets.

Martin said higher interest rates, global uncertainty and weak equity valuations have already encouraged many investors to favour fixed-income investments such as government and corporate bonds.

That means part of the Scotia payout may flow into assets outside the local stock market rather than being reinvested entirely on the JSE.

No quick replacement

Scotia’s possible departure also raises a wider question: can the JSE replace major companies when they leave?

Martin said he could not speak definitively about potential listings, but recent activity suggests a company of Scotia’s size is unlikely to be replaced quickly.

“If we use the experience of the last two years, it’s unlikely that we will get any major listings that would be able to totally replace the market cap of SGJ,” he said.

Its departure would remove roughly $184.8 billion from the JSE’s listed market capitalisation and one of the relatively few listed companies in which large investors can place significant sums while earning dividends and maintaining exposure to the financial sector.

Based on the JSE’s end-May market value and Scotia’s Tuesday closing price, the company accounts for about 10 per cent of Main Market capitalisation. Its removal would therefore take roughly one-tenth of the market’s value with it, assuming other share prices remain unchanged.

The scale of Scotia’s proposed departure is even clearer when compared with companies that have already left the market. Data reviewed by Business Observer show that 12 companies were delisted from the JSE over the past decade, with a combined market value of approximately $123.67 billion based on their market capitalisation before leaving the exchange.

At Tuesday’s closing price, Scotia’s market value of $184.8 billion was about $61.2 billion — or roughly 49 per cent — above the combined pre-delisting value of those 12 former listings.

The exchange added 16 Main Market listings over the same period, but the number of new listings alone does not show whether they replaced the market value, liquidity and investment options lost when older companies departed.

The departures included major companies such as Desnoes & Geddes, Cable & Wireless Jamaica, Scotia Investments Jamaica and Trinidad Cement, alongside others removed for non-compliance.

The Jamaica Stock Exchange did not respond to questions submitted for this story by publication time.

Why go private?

Scotiabank has said taking Scotia Group private would improve capital and operational efficiency and allow it to respond more quickly to market opportunities. It said the move would have no material effect on the Jamaican group’s current operations.

Speaking generally about privatisation deals, Martin said a majority shareholder may value having fewer public reporting requirements and greater freedom to make strategic decisions. A parent may also move to acquire the remaining shares if it believes the market is undervaluing the business.

Similar arguments have been used in earlier Jamaican takeover and delisting exercises. In the offer that preceded Cable & Wireless Jamaica’s 2018 delisting, the controlling shareholder cited low trading volumes, the premium offered to shareholders, simpler group ownership and the prospect of easing administrative and JSE compliance obligations among its reasons for buying out minority shareholders.

The Cable & Wireless offer argued that low trading volumes and a volatile share price reflected eroded shareholder value, while the cash offer would give investors liquidity and certainty.

Scotia’s transaction is structured differently, but the earlier case illustrates why a parent company may decide that fully integrating a listed subsidiary is more attractive than retaining minority shareholders and a public listing.

Scotia shares jumped $4.22, or 7.78 per cent, to $58.43 on Friday after the proposed buyout was announced. The stock added 15 cents on Monday before rising another 82 cents, or 1.4 per cent, to close at $59.40 on Tuesday. It remained $2.10 below the $61.50 offer price.

Williams said shareholders should assess the $61.50 offer against Scotia’s recent share price, earnings, book value, dividend record and future prospects once the full transaction documents and independent valuation are available.

But the decision will not be based only on valuation measures.

“Investors will also need to weigh the certainty of cash today against the potential value of continuing to participate in the future performance of the business,” Williams said.

The transaction still requires approval from minority shareholders and the Supreme Court of Jamaica.

The immediate question for shareholders is whether $61.50 is a fair price for their shares. The larger question for Jamaica’s stock market is what they can buy with the money — and what will replace Scotia once it is gone.

– This story includes contributions from David Rose

WILLIAMS…the question is not necessarily whether Scotia can be replaced by another stock, but rather whether its role within a portfolio can be replicated.