The rebuild after SSL

FSC rebuild advances but lessons document and Twin Peaks remain unfinished

THE Financial Services Commission says it has strengthened supervision following the Stocks and Securities Limited (SSL) scandal, completing hundreds of risk assessments, increasing scrutiny of off-balance sheet client assets, and beginning work on new regulatory technology.

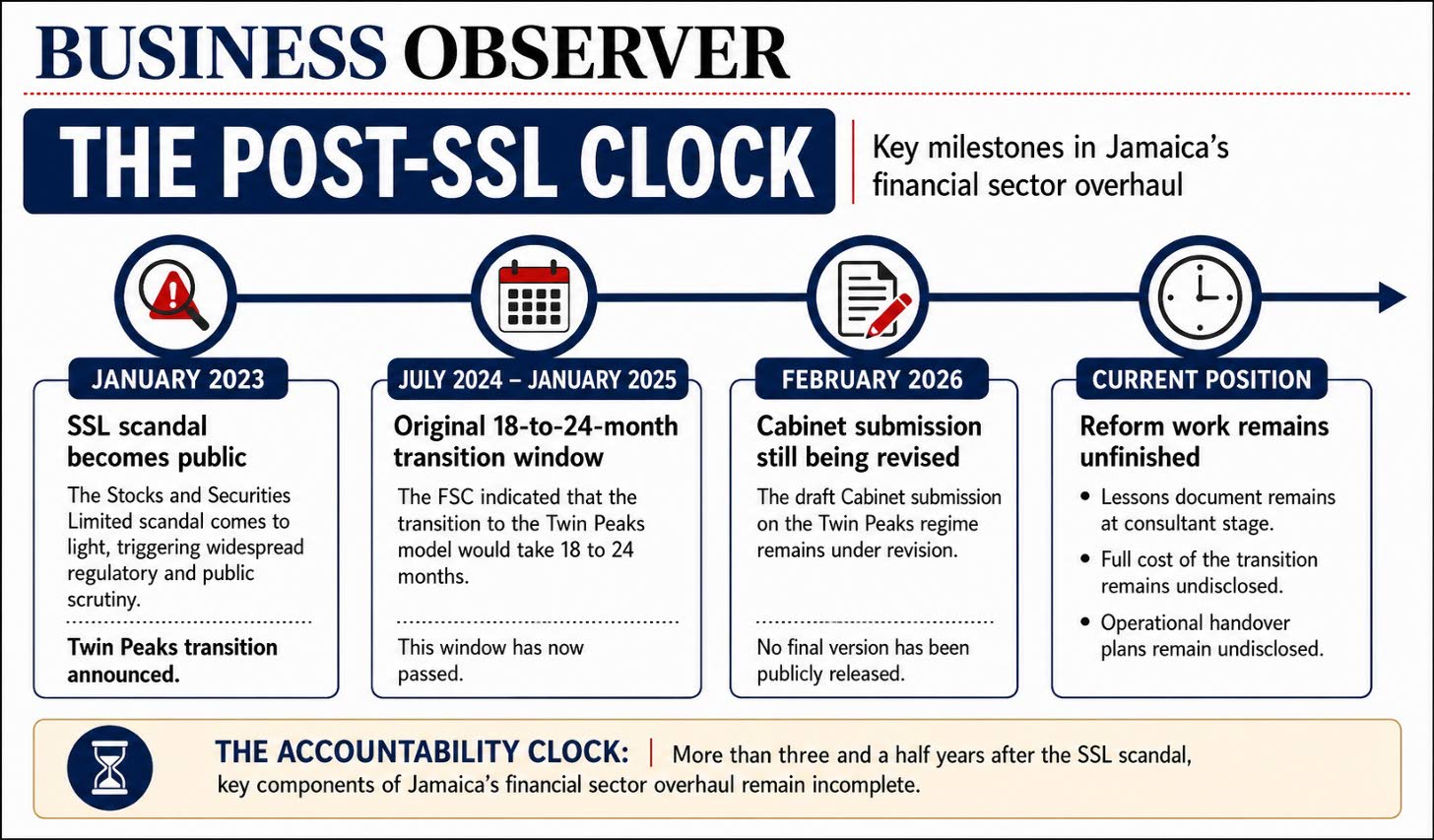

Yet, three and a half years after the scandal became public, an SSL lessons-learnt document intended to guide heightened supervision remains at the consultant stage and has not yet been implemented.

At the same time, the regulator is preparing two technology projects estimated to cost a combined US$7 million to US$10 million, while developing the market conduct, complaints resolution and consumer protection functions required for Jamaica’s planned Twin Peaks structure.

That transition has also fallen behind its original timetable. The Government initially expected the move to Twin Peaks to take 18 to 24 months, but its February 2026 Fiscal Policy Paper said the draft Cabinet submission was still being revised for circulation among government stakeholders.

Together, the unfinished lessons document, technology costs, and delayed restructuring raise the next question from SSL: What measurable improvements will the rebuilding programme produce, and when will the public be able to see them?

The work after SSL

The FSC’s 2024/25 annual report points to the creation of an additional deputy executive director position and two executive management committees, progress on cyber-risk supervision, groundwork for a joint Supervisory Technology (SupTech) project with the Bank of Jamaica, and the completion of more than 350 risk assessments across four regulated financial industries.

The report also identifies market conduct and consumer protection as increasingly important parts of the commission’s mandate.

The FSC reported a series of earlier post-SSL measures. Its 2022/23 annual report said SSL was placed under enhanced supervision and subjected to on-site examinations and additional audits. The commission also directed securities dealers to have external auditors examine off-balance sheet client assets and liabilities, and internal auditors review controls across on- and off-balance sheet product lines.

The challenge is not static. FSC data show outstanding exempt-distribution issues rising from 509 to 569 within a year, adding to the less visible parts of the market that require stronger verification, disclosure, and suitability checks.

The regulator has not disclosed when the lessons-learnt document will be completed, whether it will be published, or precisely which additional supervisory changes it is expected to trigger.

The unfinished document leaves unresolved how the FSC intends to address weaknesses raised by SSL in client-asset verification, corporate governance, regulatory escalation, and the protection of off-balance sheet investments.

The scandal also raised a more fundamental question: How long can serious weaknesses persist inside a regulated institution before intervention becomes unavoidable?

The public therefore still does not know the full set of lessons the FSC has formally drawn from SSL, what further supervisory changes will follow, or when those changes will be fully implemented.

The rebuilding is taking place as the FSC raises charges to close long-standing cost recovery gaps, making the central test not only what reform will cost but what measurable improvements the additional resources will deliver.

Millions more for technology

The next stage of the FSC’s regulatory buildout will carry a substantial price.

The regulator plans to spend approximately US$5 million on a technology system intended to reduce approval times for new financial products from as long as six months to between 30 and 45 days.

The FSC says it assesses thousands of products each year, making automation part of its effort to improve efficiency, shorten delays, and strengthen oversight.

A separate SupTech system — designed to collect, analyse, and monitor information from regulated entities — is estimated to cost between US$2 million and US$5 million.

Together, the two technology projects could require between US$7 million and US$10 million before the full cost of staffing and systems for market conduct supervision, complaints resolution, and consumer protection is established. That means the current fee increases may not represent the final cost of reform.

Twin Peaks behind schedule

The wider restructuring is tied to the Government’s planned Twin Peaks model, announced in January 2023 after the SSL scandal became public.

Under the proposed system, prudential supervision would be consolidated at the Bank of Jamaica while the FSC would become the market conduct and consumer protection regulator across the financial sector.

Twin Peaks was not created because of SSL, but the scandal gave it new urgency. Then Finance Minister Dr Nigel Clarke said the alleged fraud had “shocked the soul” of Jamaica and damaged the country’s international reputation.

The model is intended to reduce regulatory gaps, improve coordination, and separate the supervision of financial soundness from the policing of how institutions treat their customers.

The transition is expected to require amendments to several laws, the transfer or reorganisation of regulatory responsibilities, and the creation of a broader market conduct and consumer protection framework.

In January 2023 the BOJ said it was preparing its operational systems and personnel for the transition, which the Government then expected to complete within 18 to 24 months.

That original window has passed. As recently as February 2026 the Government’s Fiscal Policy Paper said the draft Cabinet submission for Twin Peaks was still being revised for circulation to government stakeholders before being submitted to Cabinet for approval.

The full cost, legislative timetable, and operational handover have not yet been clearly established publicly.

That uncertainty makes the cost and implementation of Twin Peaks part of the accountability test of whether the restructuring can deliver stronger protection and better coordination on a timetable and at a cost that are clearly disclosed and justified.

.

What does the public get?

The FSC’s 2024/25 annual report points to restructuring, risk assessments, cyber risk work and technology planning. But expenditure and staffing are inputs. Better protection is the outcome.

The records reviewed by the Business Observer do not contain a clear public framework for measuring what success will look like once the higher fees and wider regulatory reforms are implemented.

Such a framework should indicate how frequently regulated institutions will be examined, how quickly irregularities will be identified, how long complaints and enforcement cases will take to resolve, and whether the new systems will allow the FSC to verify client assets more independently and warn consumers earlier about risky or unregulated investments.

The results should also be reported publicly, allowing investors, policyholders, pension contributors and other customers to determine whether stronger supervision is actually being delivered.

The issue is not whether Jamaica needs a stronger financial regulator. After SSL, that need is difficult to dispute. It is whether the rebuilding programme is being completed, whether its promised improvements can be measured, and whether the public will be shown the results.

SSL forced Jamaica to ask whether its financial watchdog is strong enough.

A weak regulator can be far more expensive than a strong one, particularly when the price is measured in lost savings, broken trust, and damage to a country’s financial reputation.

But if Jamaica is building the regulator it wishes it had before SSL the public deserves more than announcements, new systems, and additional expenditure.

It deserves to know what is being built, when it will be completed, and whether the protection promised after the scandal is delivering results.